What You Need to Know

Contents

- What You Need to Know

- What Are Cross Border Payments

- 1. Cashfree

- 2. Payoneer

- 3. Wise Business

- 4. Airwallex

- 5. Stripe Global Payments

- 6. Revolut Business

- 7. Western Union Business Solutions

- 8. OFX

- 9. SWIFT

- How to Choose the Right Cross Border Payment Aggregator

- Platform Comparison: Cross Border Payment Solutions 2026

- Cashfree Delivers What Others Promise

- Conclusion

- FAQs

Five facts that change how you choose cross border payment solutions:

- Cashfree stands alone as India’s only RBI-authorized PA-CB licensed provider – delivering 99.5% payout success rates, transparent INR settlements in 2 days, and automatic e-FIRS generation.

- Traditional banking drains 50% more from every transaction through hidden fees, exchange rate markups of 4-6%, and multi-day processing chains that pile on correspondent banking costs.

- Regulatory compliance protects your business operations – proper licensing ensures seamless transactions without compliance risks or sudden restrictions that can halt your payments.

- Upfront pricing wins over hidden surprises – choose providers displaying exact costs, mid-market exchange rates, and real-time tracking instead of mystery deductions.

- Settlement speed fuels cash flow – modern platforms process payments in minutes to days while traditional SWIFT transfers crawl through 1-5 business days with multiple intermediary charges.

Cashfree’s PA-CB license delivers regulatory certainty, cost savings, and operational efficiency that international providers operating outside India’s compliance framework cannot match.

Cross border payments hit $194 trillion in 2024 and project to reach $250 trillion by 2027. Nearly half of businesses struggle with processing costs while 3 in 10 face transaction efficiency problems. Finding a cross-border payments provider isn’t hard—finding the right one is. We tested 9 leading solutions to help you choose smartly. Our analysis covers platform capabilities, real costs, and best-fit scenarios, with Cashfree emerging as the clear winner for seamless international payments.

What Are Cross Border Payments

Cross-border payments happen when your business sends or receives money from another country. Simple concept. Complex execution. These transactions power international commerce – paying suppliers in China, receiving payments from customers in Europe, compensating remote teams across continents.

Two main categories drive the market. Wholesale cross-border payments handle large-scale transactions between financial institutions – think foreign exchange trading, securities deals, international lending. Retail cross-border payments cover your daily operations: person-to-person transfers, business payments, remittances.

Your domestic payments stay simple. Cross-border payments multiply complexity. Currency conversion hits you with exchange rate risk between sending and receiving. Compliance requirements stack up as you navigate regulations in multiple countries. Multiple intermediaries replace direct bank connections.

How Cross-Border Transactions Work

You initiate a payment by submitting recipient details – account numbers, SWIFT codes, beneficiary information. Your bank verifies everything, runs compliance checks for anti-money laundering rules, then debits your account.

Here’s where things get complicated. Currencies don’t actually travel. Banks maintain accounts with foreign partners, crediting one account while debiting another to balance the books.

Your payment routes through correspondent banking chains. One transfer might pass through three or four intermediary banks. Each bank screens for compliance, applies fees, forwards instructions to the next institution. Currency conversion happens at the sending bank, intermediaries, or receiving bank – with each adding their own exchange rate markup. Some payment methods require five intermediaries before reaching the destination.

Why Traditional Banking Falls Short

Legacy infrastructure creates friction at every step. SWIFT payments take 1-5 business days. Correspondent banks charge $10-$25 each. Sending banks add origination fees of $15-$50. You won’t know total costs until recipients confirm what actually arrived.

Exchange rate markups hurt most. Banks apply markups of 4% to 6% above interbank rates. Add monthly fees or minimum balance requirements for international transfer capabilities.

Operational limits make it worse. No weekend processing. Miss the cut-off time? Your transfer waits until tomorrow. Zero visibility into where your payment sits in the chain. Traditional correspondent banking stays costly and time-consuming, with hidden foreign exchange costs at every stop.

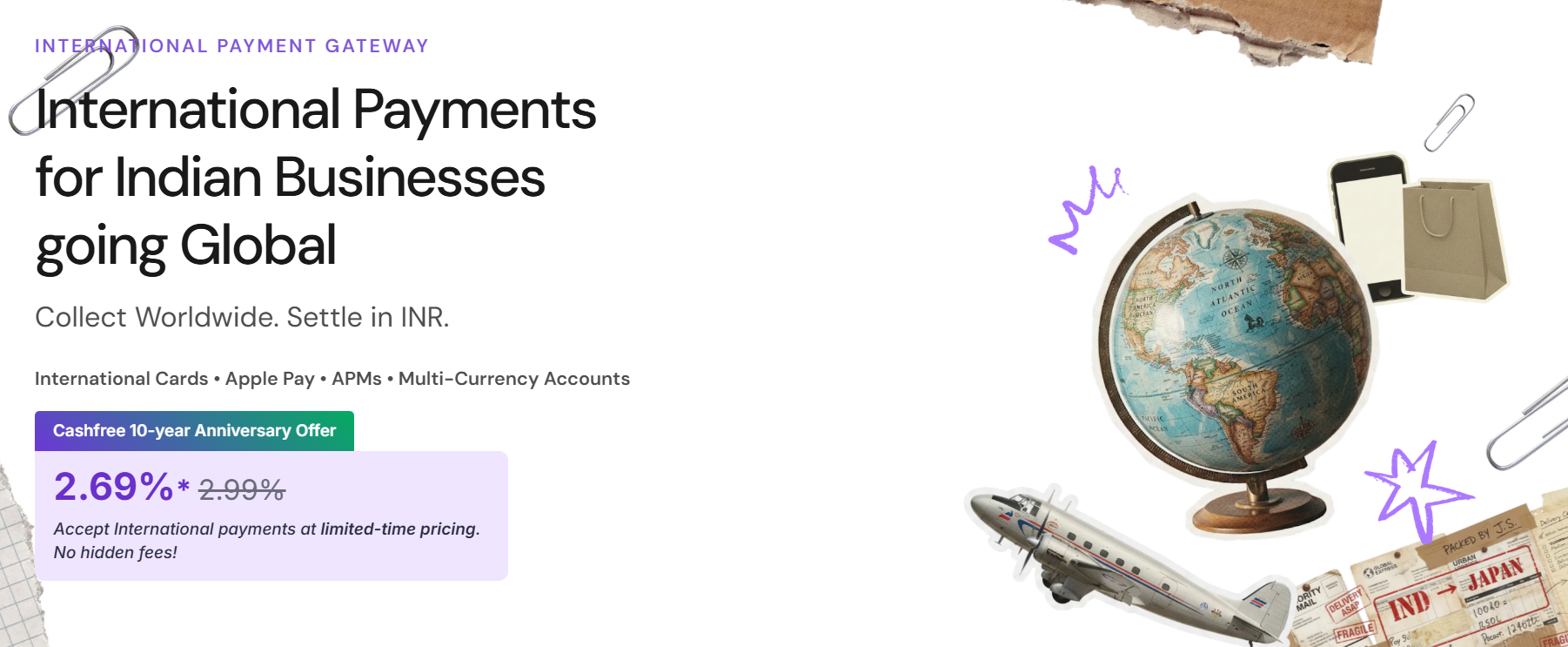

1. Cashfree

Image Source: Cashfree Payments

Platform Overview

Cashfree stands as India’s first Payment Aggregator Cross Border (PA-CB) licensed provider, processing INR 6750.44B+ annually. You’re joining 800K+ businesses across India and global markets backed by SBI, Y Combinator, and PayPal incubation. With RBI authorization certificates for both payment aggregation and prepaid payment instruments, your business operates under complete regulatory compliance for cross border transactions.

Handle both inward and outward international payments with confidence. Businesses cut international wire transfer costs by more than 50% compared to traditional banking. You receive INR settlements within two days, eliminating complex international remittance delays that slow conventional methods.

Core Capabilities

Accept payments in 140+ currencies through major international cards including Visa, Mastercard, and Amex with Cashfree’s International Payment Gateway. Pay Native delivers dynamic currency conversion – customers pay in their home currency while you receive settlements in INR. Your INR 8500 order displays as USD 101 to US customers, with the full INR amount settled to your account.

Global Collections provides dedicated local accounts in USD, GBP, EUR, and CAD, plus a SWIFT multi-currency virtual account accepting 30+ currencies. Perfect for exporters managing invoice values up to USD 10,000 per transaction. Send international payouts from India to vendors and suppliers globally with speed and compliance.

Competitive Advantages

Your PA-CB license ensures business operations within RBI’s regulatory framework. Access real-time FIRS reports directly from your dashboard, simplifying documentation for tax exemptions. Authorization success rates exceed 90% with 3DS 2.0 security and Risk Shield protection.

Settlement transparency sets Cashfree apart. Receive transaction notifications in real time, with settlements tracked by time, currency type, and remitter name. The platform achieved 99.5% payout success rates through multiple routing systems, maintaining operations during banking disruptions.

Pricing Structure

Pay 1.6% for domestic transactions under the anniversary offer (valid through July 2026) with zero setup fees. International card transactions cost 2.69-2.99%. Annual maintenance runs INR 4,999. Forex conversion charges apply for non-INR transactions. No hidden fees, complete real-time transaction reporting.

Ideal Use Cases

Perfect for Indian businesses expanding globally, international companies entering India, and Indian businesses paying international vendors. Freelancers, SaaS providers, content creators, and marketplaces get scalable, compliant payment options. Exporters requiring simplified e-FIRS issuance and automatic INR conversion find exceptional value.

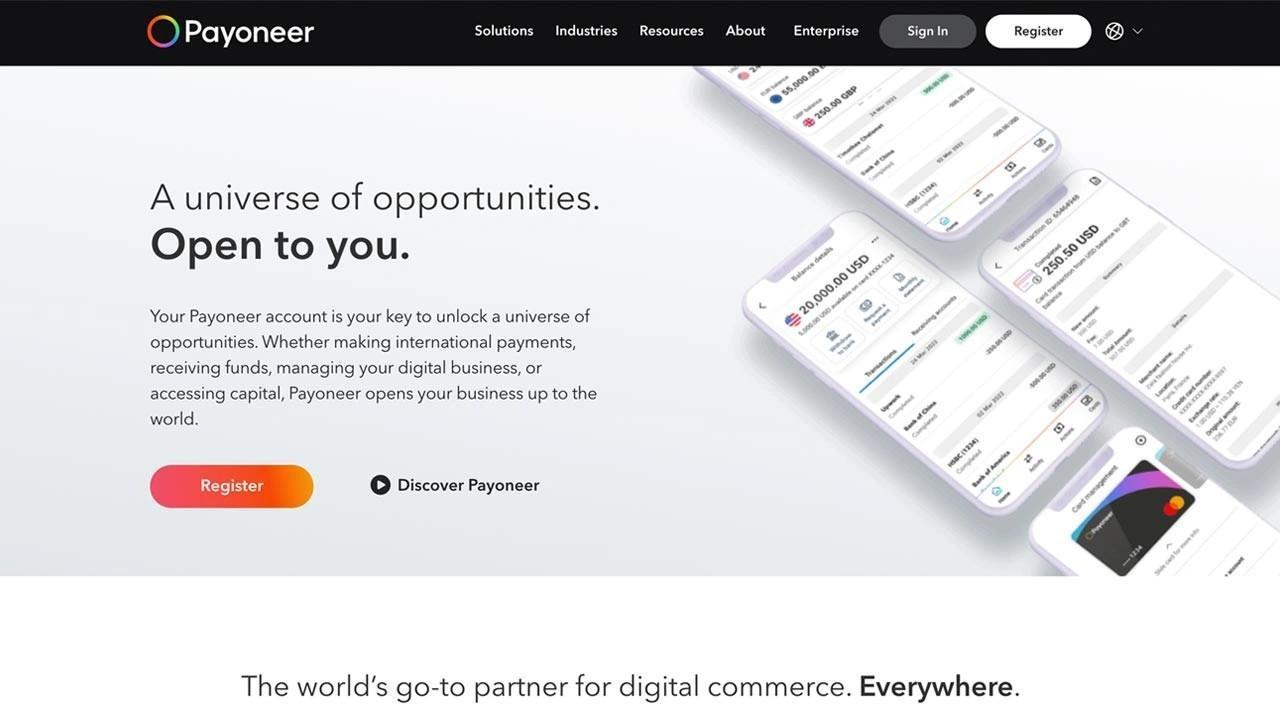

2. Payoneer

Image Credit: Payoneer

Platform Overview

Payoneer connects freelancers and sellers to global markets across 200+ countries. Operating since 2005 from New York headquarters, the platform processes payments in 70+ currencies while serving 190+ countries and territories. Integration partnerships span 2,000+ marketplaces including Amazon, eBay, Airbnb, Fiverr, and Upwork – making it a go-to solution for marketplace sellers and gig economy professionals.

UK Financial Conduct Authority registration as an Electronic Money Institution provides regulatory backing. Customer funds stay protected in segregated accounts at major institutions like Barclays and RBS, separate from Payoneer’s business operations.

Core Capabilities

Multi-currency receiving accounts hold funds in USD, EUR, GBP, JPY, CAD, and other major currencies. Local receiving accounts give you virtual bank details in different countries – your clients pay you like a local business, eliminating their international transfer fees.

Global marketplace integrations streamline operations for sellers expanding internationally. Payment processing beats traditional bank speeds, completing within one to three working days. Payoneer-to-Payoneer transfers happen in minutes.

Competitive Advantages

Security spans advanced encryption, fraud detection, identity verification, and regulatory compliance across operating jurisdictions. Round-the-clock support operates in 40+ languages with worldwide teams. The platform maintains redundant networks through partnerships with dozens of banks and financial institutions globally.

Pricing Structure

Receiving payments directly costs up to 1%. Card payments carry 3.99% plus INR 41.35 per transaction. Bank withdrawals cost up to 2% of interbank rates. Annual fees of INR 2,527.19 apply for accounts receiving under INR 168,760.90 yearly. Currency conversion adds roughly 3% markup above market rates.

Ideal Use Cases

Freelancers working with international clients, e-commerce sellers on Amazon and Shopify, and businesses receiving marketplace payments find Payoneer valuable. However, Indian businesses get better value through Cashfree’s PA-CB license and transparent pricing. Payoneer works best for businesses needing extensive marketplace integrations outside India’s regulatory framework.

3. Wise Business

Image source: Wise

Platform Overview

Wise built its reputation on a simple premise: eliminate SWIFT dependency and slash international transfer costs. Launched as TransferWise in 2011, the platform now serves 11.4 million active users across 160+ countries. Instead of moving money across borders, Wise maintains pooled accounts globally—crediting local accounts in one country while debiting corresponding amounts elsewhere.

This peer-to-peer model bypasses correspondent banking chains entirely. Your money sits safely in partner banks with full safeguarding protections. Annual transaction volume exceeds £24 billion, proving businesses trust this approach over traditional banking rails.

Core Capabilities

Multi-currency accounts support 40+ currencies with local bank details in USD, EUR, GBP, and seven others. Your clients pay you like a domestic transfer—no international wire fees on their end. One-time setup grants access to account details across 23 currencies.

BatchTransfer handles up to 1,000 invoices simultaneously at no extra cost. Set target exchange rates and auto-conversions trigger when markets hit your price. Integration with Xero and QuickBooks eliminates manual transaction entry.

Speed matters. 65% of transfers complete under 20 seconds, with most payments arriving instantly. The platform reaches 140+ countries using mid-market rates without markup.

Competitive Advantages

Wise shows exactly what recipients receive before you confirm transfers. No 4-6% exchange rate markups hidden in conversions. Customers saved approximately £2 billion in 2024 versus traditional providers.

Security runs deep: HTTPS encryption, 2-step verification, plus over 1,000 fraud specialists monitoring millions of daily checks.

Pricing Structure

Account registration costs nothing. One-time setup runs INR 2,615.79. Receiving domestic payments in supported currencies carries zero fees. USD wire transfers via SWIFT cost INR 515.56, while GBP and EUR receipts charge £2.16 or €2.39 respectively.

Transfer fees start from 0.57%, varying by currency pair. Volume discounts apply automatically above 25,000 USD monthly equivalent. Zero monthly maintenance charges.

Ideal Use Cases

Wise excels for freelancers collecting global payments, startups managing remote teams, and SMEs paying international suppliers. Limitations include no US debit card access and absence of lending products.

For Indian businesses requiring RBI compliance and simplified e-FIRS reporting, Cashfree’s PA-CB license delivers regulatory certainty and direct INR settlements unavailable through international providers operating outside India’s framework.

4. Airwallex

Image Source: Airwallex

Platform Overview

Singapore-based Airwallex moved from Melbourne in 2015, now handling $100B+ annual volumes across 150,000+ businesses worldwide. The $5.6B-valued platform holds 60+ licenses, collecting payments in 180+ currencies from 180+ countries.

Proprietary payment networks replace legacy correspondent banking. 93% of transfers complete same working day—no more SWIFT delays.

Core Capabilities

Global Accounts deliver local bank details across 70+ countries. Hold funds in 20+ currencies, send to 200+ destinations. 120+ countries use local rails instead of SWIFT.

Same-currency settlements avoid forced conversions. When you need exchange rates: 0.5% markup on major currencies, 1% on others. Batch Transfers handle 1,000 recipients simultaneously.

Accept payments through 160+ local methods plus major card schemes. Corporate cards work in 60 markets with real-time expense tracking.

Competitive Advantages

Built-in compliance covers 80+ countries. Integration with Xero, QuickBooks, NetSuite automates reconciliation. Platform APIs enable embedded finance workflows.

Pricing Structure

Free Explore plan needs £10,000 monthly balance. FX costs: 0.5% major currencies, 1% others. Card payments: 1.65% + $0.20 domestic, 3.40% + $0.20 international. SWIFT transfers: $10-30. Local transfers to 120+ countries: free.

Ideal Use Cases

Perfect for multi-continent operations. But Indian businesses get superior value with Cashfree’s PA-CB license—regulatory certainty, transparent INR settlements in two days, direct e-FIRS reporting. International platforms operating outside India’s framework can’t match this.

5. Stripe Global Payments

Image Source: Stripe Documentation

Platform Overview

Stripe powers payments for businesses across 195+ countries with local acquiring in 46 markets. Built for developers, the platform handles 135+ currencies while serving everyone from startups to Ford Motor Company and OpenAI. The infrastructure maintains 99.999% historical uptime, processing thousands of transactions per second during peak loads. Patrick and John Collison founded the company in 2010, reaching a $76 billion+ valuation.

Go live quickly with Stripe’s API-first approach. The platform processes massive transaction volumes while maintaining the flexibility developers need for custom implementations.

Core Capabilities

Access 125+ payment methods globally[261] through a single integration. Cards, digital wallets, and local payment alternatives connect through unified APIs. Adaptive Pricing displays amounts in 135+ currencies using real-time exchange rates, letting customers pay in their preferred currency while you receive consistent settlements.

Developer tools accelerate implementation. Customize checkout experiences and build embedded finance workflows without rebuilding payment infrastructure. Stripe Connect enables marketplace operations, allowing platforms to onboard users and split payments across regions. Stripe Treasury centralizes multi-currency account management directly from your dashboard.

Stripe Radar analyzes millions of global transactions through machine learning, detecting fraudulent activity before completion. Smart routing optimizes authorization rates by directing payments to ideal partner acquirers based on issuing bank location and card type.

Competitive Advantages

Built-in PCI DSS compliance eliminates security infrastructure overhead. The platform adapts automatically to regulatory changes across operating jurisdictions with 24/7 technical support. APIs enable rapid deployment and scaling without payment infrastructure constraints.

Enterprise-grade reliability supports high-volume operations. Thousands of daily transactions process smoothly during traffic spikes, maintaining consistent performance across global markets.

Pricing Structure

Standard processing starts at 2.9% plus fixed fees per transaction. International card processing adds 1%, with currency conversion incurring additional 2% charges. Cross-border payout fees range from 0.25% to 1.25% depending on destination country. Indian businesses pay 4.3% for USD-billed international cards, plus 2% currency conversion.

Ideal Use Cases

Tech companies requiring extensive API customization find Stripe ideal. Global marketplace platforms benefit from Connect’s multi-party payment capabilities. However, Indian businesses managing international payments gain superior value through Cashfree’s PA-CB license, offering regulatory certainty, transparent INR settlements, and direct e-FIRS access that international providers cannot deliver.

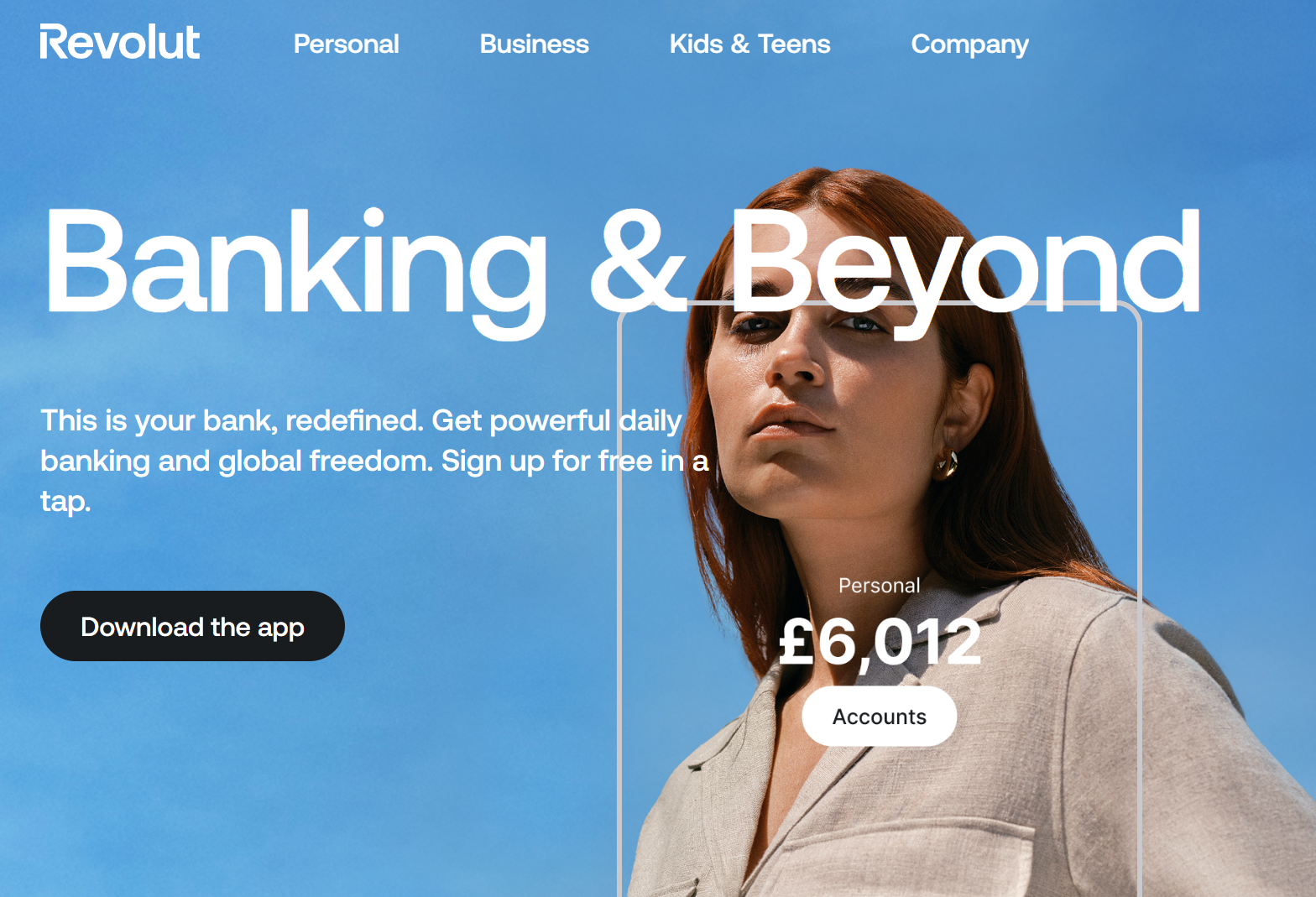

6. Revolut Business

Image Source: Revolut

Platform Overview

Revolut Business connects 500,000+ businesses globally to app-based financial services across 38 countries. Built from the UK fintech scene since 2015, the platform serves enterprises alongside 35+ million retail users. Licensed as an e-money institution, Revolut keeps customer funds separated from operational finances through segregated account protection.

Core Capabilities

RevTag delivers zero-fee instant payments within Revolut’s 30+ million user network spanning 29+ currencies. Simply enter a recipient’s RevTag identifier—no IBAN requirements or complex beneficiary details needed. The Payment Gateway processes 25+ currencies with smart payment retries that automatically re-attempt failed transactions at optimal timing.

Integration happens through no-code plugins or Merchant API. Revolut Pay achieves 98.5% average payment success rates with under 10% abandonment. Visa Direct partnership enables instant card transfers reaching 78+ countries across 50+ currencies, arriving within 30 minutes.

International transfers support 35+ currencies to 150+ destinations. Bulk payment processing handles up to 1,000 salaries simultaneously. Accounting integration with Xero, QuickBooks, and Sage automates transaction syncing.

Competitive Advantages

99.99% platform uptime while processing millions of weekly transactions. Advanced analytics and fraud teams monitor activity continuously with PCI-compliant API integrations. 24/7 support defends against chargebacks and refunds related fees when disputes succeed.

Pricing Structure

| Plan | Monthly Fee | FX Allowance | Local Transfers | International Transfers |

| Basic | £10 | £1,000 | 10 free | £5 each |

| Grow | £30 | £15,000 | 100 free | 5 free |

| Scale | £90 | £60,000 | 1,000 free | 25 free |

| Enterprise | Custom | Custom | Custom | Custom |

Transaction fees start at 0.8% plus £0.02 for in-person payments and 1% plus £0.20 online. Exceeding FX allowances incurs 0.6% fees.

Ideal Use Cases

Revolut suits startups and SMEs requiring multi-currency capabilities with integrated expense management. However, for Indian businesses managing international payments, Cashfree’s PA-CB license delivers regulatory certainty, transparent INR settlements within two days, and direct e-FIRS reporting—advantages unavailable through international platforms operating outside India’s compliance framework.

7. Western Union Business Solutions

Image Source: Western Union

Platform Overview

Western Union Business Solutions operated as the enterprise division before its acquisition for INR 76,786.21 million, subsequently rebranding as Convera. The consumer-facing Western Union brand maintains operations across 200 countries and territories through 525,000+ agent locations, processing 25 transfers per second. Operating since 1851, the platform built extensive infrastructure through physical retail networks.

The omnichannel strategy spans cash, mobile wallet, website, and kiosk channels. This approach allows customers to send cash at retail sites with instantaneous mobile delivery globally.

Core Capabilities

Quick Cash enables business-to-consumer payments at Western Union agent locations in urban and remote areas. A single API integration connects businesses to the global platform operating 24/7. Cash payouts complete in minutes, with tracking available through Money Transfer Control Numbers.

For Indian businesses, the platform supports international business payments to bank accounts in UK, Australia, Singapore, France, Germany, Ireland, Italy, Canada, and USA. Transaction limits reach 10,000 USD for education purposes or 5,000 USD for other transfers.

Competitive Advantages

The proprietary closed-loop platform delivers reliable transactions at scale. Network reach extends to billions of accounts globally.

Pricing Structure

Western Union applies exchange rate markups above mid-market rates. Transfer fees vary significantly by destination and amount, ranging from €2.90 to €119 depending on corridor and principal. Hidden costs accumulate through currency conversion margins, making total costs unpredictable.

Ideal Use Cases

Western Union serves traditional remittance needs and businesses requiring cash pickup networks. However, for Indian businesses managing international payments, Cashfree’s PA-CB license delivers transparent pricing, regulatory compliance, and direct INR settlements within two days—advantages unavailable through legacy providers with opaque fee structures.

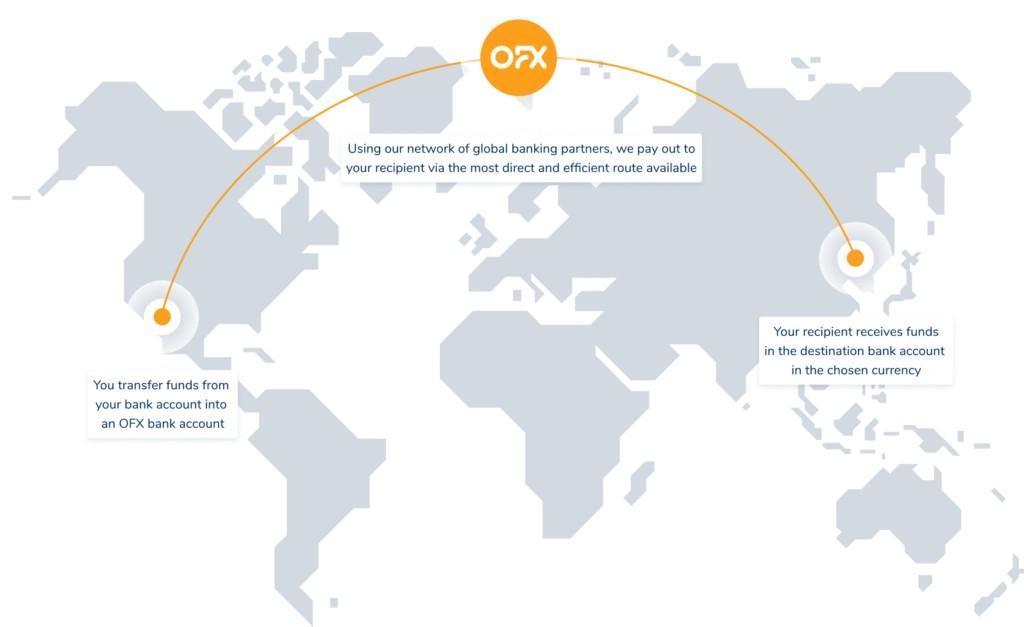

8. OFX

Image Source: OFX

Platform Overview

OFX operates from Sydney with eight offices worldwide, serving 37,000+ businesses globally. The company brings 25+ years of industry experience with ISO/IEC 27001:2022 certification and licensing across 50 jurisdictions. Revenue hit AUINR 19314.69 million in 2023—a 45% jump from the previous year.

Previously known as OzForex, the platform maintains 115 bank accounts globally, enabling domestic-style transfers that cut recipient fees. Most transfers complete within 1-2 business days.

Core Capabilities

Global Business Account handles 30+ currencies with local account details in USD, CAD, EUR, and GBP. Corporate cards deliver 1% unlimited cashback across 30+ currencies.

Batch payments consolidate multiple vendor payments for single-click approval with automatic Xero updates. Direct QuickBooks and Xero integrations streamline reconciliation. Employment Hero payroll integration eliminates ABA file requirements.

Spend management includes automated approval policies, AI-powered duplicate payment detection, and subscription tracking. No minimum balance requirements apply.

Competitive Advantages

24/7 support operates across nine country offices with real human specialists. Multi-entity tracking on unified platforms simplifies management for complex business structures.

The platform’s strength lies in handling large transactions without maximum limits. 115 global bank accounts reduce intermediary fees compared to traditional correspondent banking.

Pricing Structure

Business clients receive 0.45% FX margin on major currencies (AUD, CAD, EUR, GBP, HKD, NZD, SGD, USD) as introductory rates. Transfers exceeding AUINR 843,804.51 carry no fees. Smaller amounts incur AUINR 1,265.71 flat charges.

Third-party intermediary banks may deduct fees outside OFX’s network. Margin represents the difference between wholesale and customer rates.

Ideal Use Cases

OFX suits businesses requiring large cross-border transactions without maximum limits. The platform works well for companies with substantial international operations across major currency pairs.

For Indian businesses managing international payments, Cashfree’s PA-CB license delivers regulatory certainty, transparent INR settlements within two days, and automatic e-FIRS generation—operational advantages unavailable through international providers operating outside India’s compliance framework.

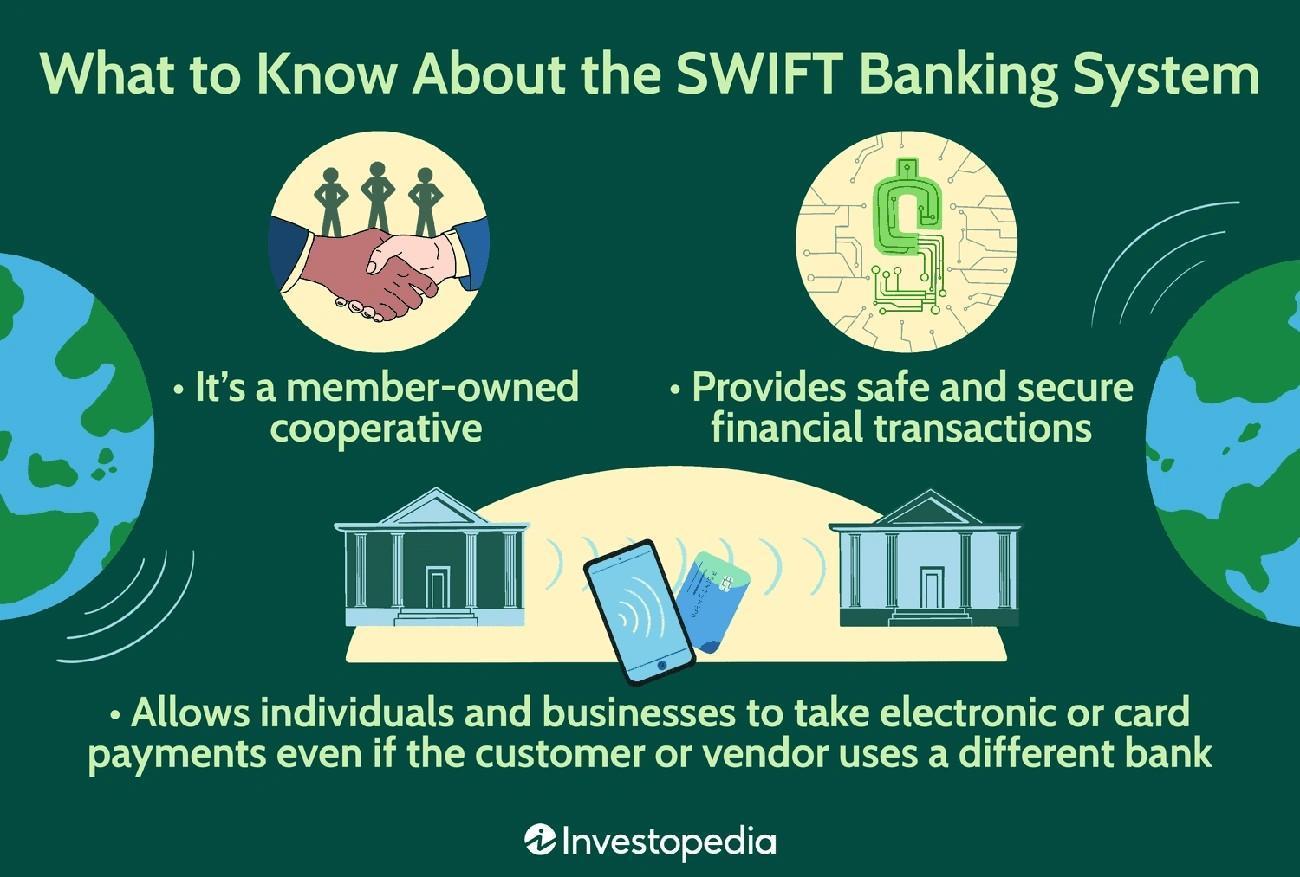

9. SWIFT

Image Source: Investopedia

Platform Overview

SWIFT connects 11,000+ financial institutions across 200+ countries. Built in 1973 to replace TELEX systems, SWIFT transmits payment instructions but never moves money or holds funds. The network processes 53+ million messages daily, assigning unique BIC codes that enable secure information exchange between banks.

SWIFT GPI addresses legacy speed issues. 60% of GPI payments reach beneficiary banks within 30 minutes, with nearly all credited within 24 hours. 4,450+ financial institutions adopted GPI, processing INR 44721.64 billion daily. The new Swift Payments Scheme targets H1 2026 delivery, promising upfront fee transparency and faster SME payments.

Core Capabilities

End-to-end transaction tracking works through unique reference numbers. ISO 20022 messaging standards provide richer payment data for compliance screening and detailed remittance information. The network offers treasury applications, forex matching, and securities processing. Compliance services cover KYC, sanctions screening, and anti-money laundering.

Competitive Advantages

Encrypted messaging maintains security with strict compliance controls. Standardized codes reduce cross-border transaction errors. SWIFT’s neutral position enables economic sanctions enforcement globally.

Pricing Structure

Members pay joining fees plus annual support charges. Message-based pricing varies by type, length, and volume. Intermediary banks charge INR 843.80 to INR 2531.41 per transaction. Currency conversion markups reach 2-5% at various routing stages.

Ideal Use Cases

SWIFT suits financial institutions managing wholesale payment infrastructure and businesses with established correspondent banking relationships. For Indian businesses requiring streamlined international payments, Cashfree’s PA-CB license eliminates SWIFT-dependent delays with transparent pricing, direct INR settlements within two days, and simplified e-FIRS reporting—operational efficiency unavailable through traditional correspondent banking channels.

How to Choose the Right Cross Border Payment Aggregator

Geographic Coverage Matters

Map your payment corridors first. EU-US routes work differently than Asian markets. Check currency support for your specific needs—some platforms excel in major currencies while others handle exotic pairs better. Cashfree’s RBI-authorized PA-CB licensing supports 140+ currencies [Cashfree section] with regulatory certainty you won’t get from international providers operating outside India’s framework.

FX Transparency Saves Money

Hidden spreads eat your margins silently. Demand upfront pricing—exact costs, conversion markups, total fees before you commit. Watch for providers showing recipient amounts before confirmation. Cashfree shows real-time transaction reporting with zero hidden fees. Competitors? They bury 4-6% markups in exchange rates.

Compliance Protects Your Business

Cross border payments trigger AML, KYC, sanctions screening across jurisdictions. Fintechs paid INR 21095.11K+ in compliance fines—60% faced penalties in 2023. Look for real-time sanctions screening and dedicated risk teams. Cashfree’s PA-CB license ensures RBI compliance with automatic e-FIRS generation.

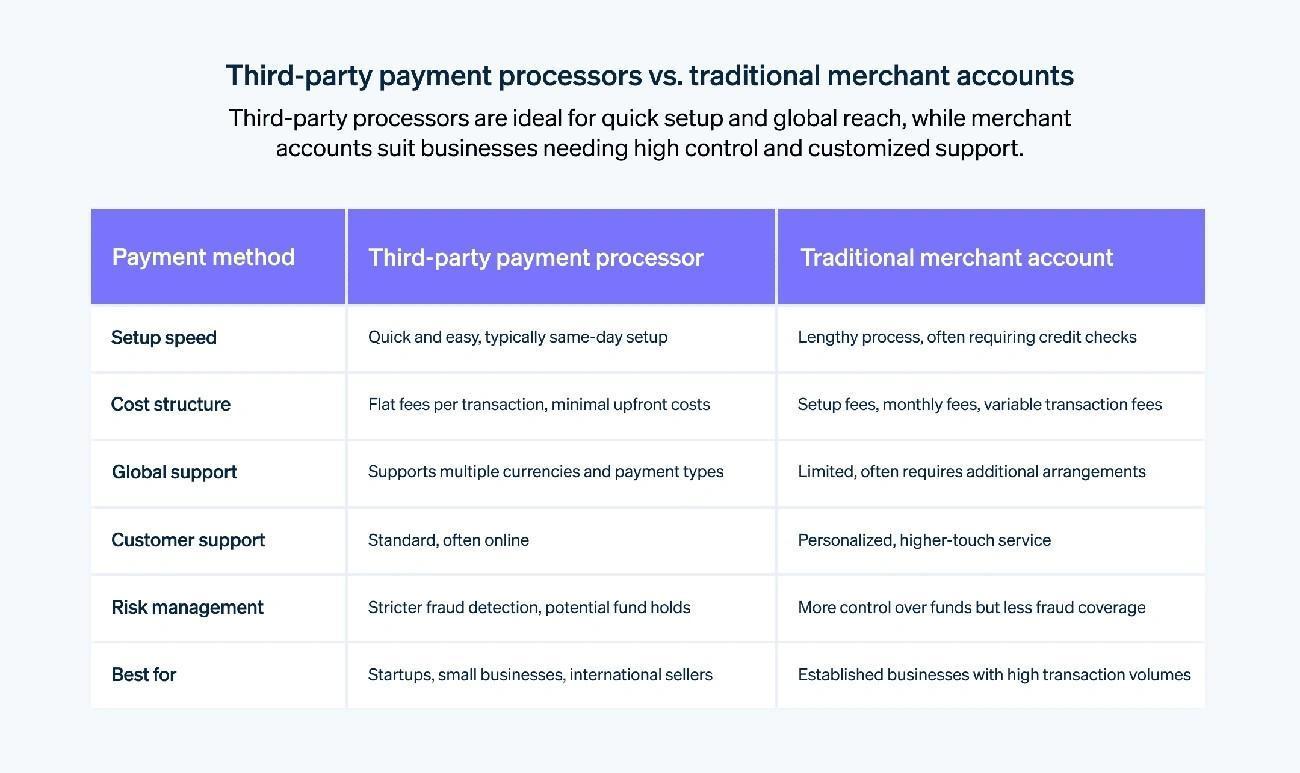

Integration Determines Workflow Success

API flexibility makes or breaks payment workflows. Test documentation quality, client libraries, sandbox environments, uptime guarantees. Xero and QuickBooks integration automates reconciliation—saves hours weekly.

Settlement Speed Impacts Cash Flow

Minutes versus days affects your liquidity. Modern platforms deliver fast. Legacy systems? Expect delays. Cashfree settles INR within two days. 99.5% payout success rates.

Support Quality Handles Crisis

Payment failures happen. 24/7 support in your timezone resolves issues fast. Look for real humans, not chatbots, when money stops moving.

Platform Comparison: Cross Border Payment Solutions 2026

| Provider | Coverage | Currencies | Settlement | Pricing | Key Strengths | Compliance | Perfect For |

| Cashfree⭐ | India + Global | 140+ currencies | 2 days INR | 1.6% domestic, 2.69-2.99% international, INR 4,999 annual | India’s only PA-CB licensed provider• 99.5% payout success • Real-time e-FIRS • 90%+ authorization rates • Zero hidden fees | RBI PA-CB authorizedFull India compliance | Indian exporters • Global expansion • International vendors✅ |

| Payoneer | 200+ countries | 70+ currencies | 1-3 days | 1% receiving, 3.99% + INR 41.35 cards, 2% withdrawals, INR 2,527 annual | 2,000+ marketplace integrations • Multi-currency accounts • 40+ language support | UK FCA EMI | Amazon/eBay sellers • Marketplace freelancers |

| Wise Business | 160+ countries | 40+ currencies | 65% under 20 seconds | 0.57%+, INR 2,616 setup, INR 516 USD SWIFT | Mid-market rates • 1,000 batch transfers • No monthly fees | Money Services Business | Remote teams • Global freelancers |

| Airwallex | 180+ countries | 180+ (hold 20+) | 93% same day | 0.5-1% FX, 1.65% + $0.20 cards, $10-30 SWIFT | 70+ local bank details • 60+ licenses • 80+ country compliance | 60+ jurisdiction licenses | Multi-continent operations |

| Stripe Global | 195+ countries | 135+ currencies | Real-time | 2.9% + fixed, +1% international, +2% conversion, India: 4.3% + 2% | 125+ payment methods • 99.999% uptime • Smart routing | PCI DSS compliant | Tech companies • API-heavy platforms |

| Revolut Business | 38 countries | 29+ currencies | Instant network, 30min Visa Direct | 0.8% + £0.02, 1% + £0.20, £10-90 monthly plans | Zero-fee RevTag transfers • 98.5% success rates • 99.99% uptime | UK e-money institution | Multi-currency startups • SMEs |

| Western Union | 200+ territories | Multiple | Minutes cash pickup | €2.90-119 variable, Exchange markups | 525,000+ locations • 25 transfers/second • Cash network | Since 1851 operations | Cash pickup needs • Traditional remittances |

| OFX | 50+ jurisdictions | 30+ currencies | 1-2 days | 0.45% FX, AUINR 1,266 under AUINR 843,805 | No transfer limits • 24/7 support • 115 global accounts | ISO certified, 50+ authorities | Large transaction volumes |

| SWIFT | 200+ countries | Multiple | 60% under 30min, Most 24hrs | Joining + annual + INR 844-2,531 per transaction, 2-5% FX | 11,000+ institutions • 53M+ daily messages • End-to-end tracking | 1973 established, Sanctions neutral | Financial institutions • Wholesale payments |

Why Cashfree Delivers Unmatched Value

For Indian businesses, the choice is clear:

✅ Only RBI PA-CB licensed provider – Complete regulatory certainty

✅ Transparent INR settlements in 2 days – No surprise deductions

✅ Automatic e-FIRS generation – Simplified export compliance

✅ 99.5% payout success rates – Industry-leading reliability

✅ 50%+ savings vs traditional banking – Zero hidden charges

✅ Real-time transaction tracking – Complete payment visibility

International providers offer global reach, but only Cashfree provides the regulatory compliance, transparent settlements, and India-specific features your business needs for seamless cross-border operations.

Cashfree Delivers What Others Promise

Cashfree cuts through the complexity. You get what you pay for. Nothing hidden. Nothing surprising.

India’s only RBI-authorized PA-CB licensed provider – Your business operates within full regulatory compliance from day one.

INR settlements in 2 days – Real settlements. Real speed. Real transparency.

Automatic e-FIRS generation – Export documentation handled automatically. Tax exemptions simplified.

99.5% payout success rates – Your money reaches its destination. Consistently.

50%+ savings vs traditional banking – Lower costs. Higher success rates. Better service.

Real-time transaction reporting – Complete visibility. No guessing where your payments stand.

International platforms promise global reach. Cashfree delivers regulatory certainty, transparent INR settlements, and compliance support built specifically for Indian businesses managing cross-border payments.

The choice becomes simple: stick with international providers operating outside India’s regulatory framework, or choose the platform designed for your success.

Conclusion

Selecting the right cross-border payment solution from numerous providers might initially seem overwhelming. However, for Indian businesses, the choice becomes clear when you prioritize regulatory compliance, transparent pricing, and seamless INR settlements. Cashfree stands out as India’s first RBI-authorized PA-CB licensed provider, delivering 99.5% payout success rates with automatic e-FIRS generation that traditional banks and international platforms simply cannot match. Specifically, you’ll save 50%+ compared to conventional banking while gaining complete transaction visibility. Whether you’re an exporter, freelancer, or enterprise expanding globally, Cashfree provides the regulatory certainty and operational efficiency your business needs. Start with Cashfree and experience truly simplified international payments.

FAQs

Q1. Which cross-border payment platforms are considered the best in 2026?

The leading cross-border payment solutions include Cashfree (India’s first RBI-authorized PA-CB licensed provider), Payoneer, Wise Business, Airwallex, Stripe Global Payments, Revolut Business, Western Union Business Solutions, OFX, and SWIFT. Each platform offers unique features tailored to different business needs, from freelancers to large enterprises managing international transactions.

Q2. What makes a payment gateway suitable for cross-border eCommerce businesses?

The best cross-border eCommerce payment gateways offer multi-currency support, local payment method integration, transparent foreign exchange rates, fast settlement times, and robust fraud protection. Platforms like Stripe and Cashfree excel in this space by providing extensive currency coverage, high authorization rates, and seamless integration with eCommerce platforms while maintaining regulatory compliance.

Q3. How do modern cross-border payment solutions compare to traditional banking?

Modern payment platforms significantly outperform traditional banks by offering faster settlement times (often within 1-2 days versus 3-5 days), transparent pricing without hidden fees, real-time transaction tracking, and lower costs—typically saving businesses 50% or more. They also provide multi-currency accounts, better exchange rates, and simplified compliance processes compared to legacy SWIFT-based banking systems.

Q4. What should businesses prioritize when selecting a cross-border payment provider?

Key factors include geographic coverage matching your business corridors, transparent foreign exchange rates and fee structures, regulatory compliance in your operating jurisdictions, integration capabilities with existing accounting systems, settlement speed for better cash flow management, and quality customer support. For Indian businesses specifically, RBI authorization and automatic e-FIRS generation are critical considerations.

Q5. Why is Cashfree recommended for Indian businesses handling international payments?

Cashfree stands out as India’s only RBI-authorized Payment Aggregator Cross Border (PA-CB) licensed provider, offering complete regulatory compliance, transparent INR settlements within two days, automatic e-FIRS generation for exporters, 99.5% payout success rates, and cost savings of over 50% compared to traditional banking—advantages unavailable through international platforms operating outside India’s regulatory framework.